Offsetting an X% Loss in Your Portfolio Requires a Greater than X% Gain

It's simple but sometimes confusing math

I recently wrote an article about how it is important to minimize losses in your portfolio and provided a few tools to limit the magnitude of those losses:

In today’s article, I want to show the simple math that underpins why this is important: it is because you need a larger than X% increase in your investment to make up for an X% loss. Even worse, the percentage gain you need to make to get back to even grows as the magnitude of the decline increases.

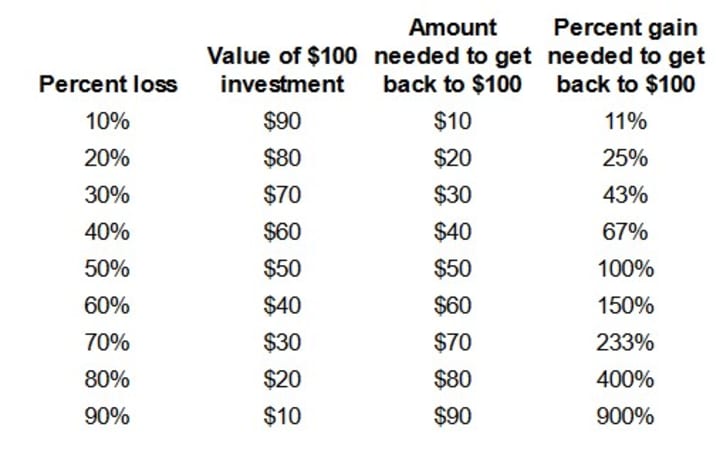

Here is a chart to illustrate that simple math. I’ve used a hypothetical $100 investment. Each row shows how much money you have left after a specified percentage loss, how much money to you need to earn to get back to even and then the percentage gain from your remaining money that it entails:

Hopefully, the two items I outlined above clearly pop out when you look at the chart:

- Anytime you have a loss, you need a greater percentage gain to offset that loss. So, for example, if you lose 20% on your investment (the second row of data in the chart), you need a 25% gain to get back to even

- As the magnitude of losses increases, there is an accelerating growth in percentage gains to get back to even. It takes a 100% gain to get back to even from a 50% loss. If that loss grows by 10% to 60%, you need a 150% increase to get back to even. The difference between the percentage loss and percentage gain needed to get back to even increases as the loss increases

Why does this matter?

It’s important to keep an eye on all of your investments. As human beings, we have a natural tendency to focus on those investments where we are earning money and mentally mute those where we are losing. Even more, when we do look at those where we are losing, we have a deep down belief that the investment will come back to break even.

As the chart above shows, its gets harder and harder on a percentage basis to come back to even as losses increase. Because of this, the ability to find a way to differentiate between investments which are declining within the bounds of investments’ normal variability vs. those which are at the beginning of a more serious decline can make a serious difference in the overall return of your portfolio.

So what can I do?

In an ideal world, you’re already using the tools I outlined in my previous article. Those help you keep investments which are going through normal variability while cutting your losses short once the investment goes down by a larger than acceptable percentage.

Even if you are using the tools, it is worth your time to look at investments which have decreased in value, but not yet to the level where those tools automatically sell the investment — as you periodically review your portfolio, you should look deeper at the investments which have decreased in value beyond a lower threshold. I use a 10–15% decrease as a rule of thumb to identify investments which might be going past normal amounts of variability. Once I’ve identified those, I relook at the initial thesis that drove me to invest in that asset.

If the thesis remains valid, I might actually invest more in that asset as it’s on sale compared to when I originally bought it. This way, I’m lowering my average cost while still expecting the longer term value that I initially expected. However, if something has changed and the original thesis is no longer valid, it’s time to move on or reduce the size from this investment and I start selling. This way I can prevent further and growing damage from the asset. Taking this action now further reduces the likelihood that I will end up with a larger loss and the big gains necessary to get back to even.

This completes today’s post on Offsetting an X% Loss in Your Portfolio Requires a Greater than X Gain. The practical steps you can start taking from today’s post are:

- Pay attention to the parts of your portfolio that are going down as well as up: It’s natural as a human being to focus on the parts of your portfolio that are gaining and gloss over those that are declining.

- Do all that you can to minimize your losses: Use tools such as the ones I mentioned in my article on Minimizing Losses to Maximize Your Portfolio’s Return. By limiting the magnitude of your losses, you prevent yourself from having to earn many hundreds of percent gains on those losing investments to break even.

- Recognize that as investments decline more in value, the percentage gain you need to make to get back to even increases at a faster and faster rate: This is simple math and is why you need to cut off investments which are likely to decline more as quickly as possible.

- Review your thesis for investing in assets where the loss is greater than 10-15%: When an investment falls in value, you should look at your investment thesis and see if it is still valid. All investments rise and fall in value, so don’t worry about investments which have small declines. Once the decline becomes meaningful — I use 10–15% as that threshold — recheck your thesis. If the thesis is still valid, this might be an opportunity to invest more and lower your average cost basis. However, if the thesis is not valid anymore, sell out of that investment or reduce its share in your portfolio and minimize further losses.

- Please also note that I am not a financial advisor and I am sharing what I do with investments for information and educational purposes only: Do your own due diligence before you make any investment decisions

Thank you for joining me on my journey to build financial literacy for young adults and their families. Please share any comments or questions that you have in the comments section. If you are interested in reading more of my posts, please access my author page (https://vocal.media/authors/sudhir-sahay) where you can see all the posts I’ve published. Also, if there are any topics you’re interested in my broaching in future posts, please let me know. In addition to the comments section, I can be reached at [email protected].

About the Creator

Sudhir Sahay

Sudhir Sahay is a Sales and Marketing executive and a father of two young men. Sudhir hopes to share his journey building basic financial literacy for his children and providing savings and investing advice to their friends and peers.

Keep reading

More stories from Sudhir Sahay and writers in Trader and other communities.

Increase your Sales Price and Profit by Selling Stocks with Covered Call Options

Bull low, sell high. That’s the holy mantra for investors who want to maximize return. But, how do you do that? Last week, I wrote an article about how to reduce your entry point for investments — i.e, buy low — using put options.

By Sudhir Sahay2 months ago in Trader

Once More Unto The Breach

He let the sword slip through his other gauntleted hand. Athlistan stood atop the crest of the rubble of Bordanium’s ruptured curtain wall. Beyond, the remnants of the Saxon’s first assault regrouped. They would come again–Athlistan knew it.

By Matthew Fromm5 days ago in Fiction

Devoured

My fingers dance across the yellowed pages of the library’s archaic volumes. Despite the candle illuminating the shelves, I’m not searching for a book. Instead, I’m relentlessly investigating the halls for a door to run from the horrible reality that consumed all our lives.

By Isabella Rose5 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.